Popular Personal Insurance policies and their differences (Term/Health/ULIP)

Insurance Policies - Popular Personal Insurance policies and their differences (Term/Health/ULIP) in Personal Finance - Term insurance, Health Insurance and ULIP are the most popular personal insurances that people buy. Each of them cover one ...

Popular Personal Insurance policies and their differences (Term/Health/ULIP)

Term insurance, Health Insurance and ULIP are the most popular personal insurances that people buy. Each of them cover one aspect of insurance and are deemed necessary by people for their own reasons. Main objective of an insurance is to protect the policyholders during emergencies. Emergencies can be of different forms and so different types of insurance products are available.

One need to understand each of them in detail and take an informed decision before buying an insurance policy. At times, there will be lot of mis-selling to spike up premiums. This article aims to create awareness about these policies and their differences. Before we compare these insurances, let us understand each one of them first.

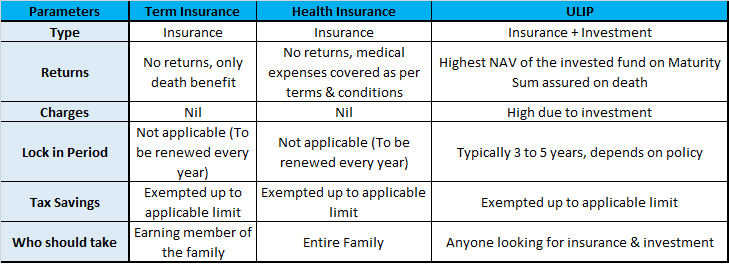

Term Insurance

Term insurance is the simplest and purest form of life insurance policy where the premium is entirely for covering the life of the policyholder. There is no maturity benefit in a term insurance policy. Sum assured is paid to the nominee in the unfortunate demise of the policyholder during the policy period. This is a cost-effective insurance with a higher sum assured.

Health Insurance

Health Insurance covers individual or family against the medical expenses that arise due to illness. Medical expenses keep increasing year after year and having a comprehensive health insurance will take care of hospitalization expenses and helps in significant amount of savings/push someone into financial distress that otherwise would have been spent for medical expenses.

Unit Linked Insurance Plan (ULIP)

ULIP has investment part apart from insurance under a single integrated plan. Part of the premium paid is invested. ULIP has both death AND maturity benefit. Since investment is present in this policy, there will be significant charges. Investors have option to select where the fund need to be invested.

Now that we have briefly know about the nature of these insurance policies, let us do a comparison of these three under various parameters.

Conclusion:

For those looking to safeguard their dependent family members when they are not around, TERM INSURANCE is the best one to go for as it gives high sum assured for low premiums. One should take sum assured as at least 10 times their annual pay and have coverage until they are 60 years old. At least family members will not be financially troubled. Plain term insurance is enough without any RIDERS like critical illness cover, as health insurance will take care of it. Never mix insurance purposes; otherwise, you will end up paying more premium.

Unplanned emergency will be mostly related to health. Given the current life style and food habits, having a health insurance becomes necessary for all. Though salaried employees get cover through group plans, it is advisable to have a personal health coverage (now porting/converting is made possible through regulations). Think about health inflation 10, 20 years down the line. So do not just take coverage for amount required at current time. Go for higher coverage like 15L a year for a family floater plan. Premiums will be around 20,000 a year. Have a separate cover for parents, as they are more prone to have medical issues with old age.

Most people feel that they may outlive the policy period in term insurance and so the premiums paid towards term policy is considered as a LOSS. This makes people to look for a combination of insurance and investment. Insurance providers use this pitch to sell an integrated product, ULIP that offers both insurance as sum assured on death and returns on maturity. However, watch this video to know why I say one should NOT mix insurance and investment. Returns generated are even less than FD and sum assured is nowhere near to even one year pay which will be of no help to dependent family. AVOID ULIP

Register To Reply

Register To Reply